How it works

Medicare Supplement (Medigap)

Works alongside Original Medicare (Part A & B)

Medicare Advantage (Part C)

Replaces Original Medicare with a private plan

Understanding Medicare can be confusing, especially when trying to decide which coverage options are right for you. This guide provides a clear, easy-to-understand overview of Medicare, including what each part covers, who pays for it, enrollment periods, and supplemental coverage options.

Medicare Part A helps cover inpatient hospital care and related services.

What Medicare Part A covers: - Inpatient hospital stays, skilled nursing facility care, hospice care, limited home health services

Who pays for Medicare Part A: Most people qualify for premium-free Part A if they or their spouse paid Medicare taxes for at least 40 quarters (10 years).

Medicare Part B covers medically necessary outpatient services and preventive care.

What Medicare Part B covers: - Doctor visits and specialist appointments, outpatient services, preventive care and screenings, lab work, imaging, and durable medical equipment

Who pays for Medicare Part B: Part B requires a monthly premium paid by the beneficiary. The premium is based on household income. Higher-income individuals may pay an additional amount called IRMAA (Income-Related Monthly Adjustment Amount).

https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

Important Part B Enrollment Notice:

If you do not enroll in Medicare Part B when you are first eligible and do not have creditable employer group health coverage, you may be subject to a late enrollment penalty. This penalty is added to your monthly Part B premium and generally lasts for as long as you have Part B.

Medicare Advantage plans (Part C) are offered by private insurance companies to help limit a member’s out-of-pocket liability under Medicare Part A and Part B.

What Medicare Advantage plans include: All benefits provided under Medicare Part A and Part B, and include Medicare Part D prescription drug coverage, creating a single, well-rounded health plan. Additional benefits can include dental, vision, hearing, fitness, wellness programs. Copays and out-of-pocket costs vary by plan.

Who pays for Medicare Advantage: Some plans have $0 or low monthly premiums. Members must continue to pay their Medicare Part B premium.

Network Access: HMO, POS, HMO

Medicare Part D helps cover the cost of prescription medications.

What Medicare Part D covers: - Outpatient prescription drugs

Who pays for Medicare Part D: Monthly premium paid by the member. Premiums vary by plan and carrier. Higher-income individuals may pay an income-based surcharge

*Part D coverage can be included with a Medicare Advantage plan or purchased as a stand-alone plan alongside Original Medicare.

Medicare Part D Late Enrollment Penalty: If you go without creditable prescription drug coverage for 63 days or longer after you are first eligible, you may have to pay a late enrollment penalty. This penalty is added to your Part D premium and generally applies for as long as you have Medicare drug coverage.

Medicare Supplement (Medigap) plans are designed to work alongside Original Medicare (Part A and Part B) to help reduce out-of-pocket expenses.

What a Medicare Supplement helps cover: Deductibles, coinsurance, copays that are not fully paid by Medicare.

Who pays for Medicare Supplement: Premiums are typically age-rated and may be gender-specific. Members must continue to pay their Medicare Part B premium. Copays and out-of-pocket costs vary by plan.

Network Access: Any provider who accepts Medicare.

*Medicare Supplement plans do not include prescription drug coverage.

Enrolling during your Initial Enrollment Period helps avoid late enrollment penalties.

January 1 through March 31 each year

October 15 through December 7 each year

Special Enrollment Periods may be available if you experience a qualifying life event, such as:

Medicare is a federal health insurance program for individuals age 65 and older. In some cases, you may qualify for Medicare before age 65 if you have a qualifying disability, End-Stage Renal Disease (ESRD), or ALS (also known as Lou Gehrig’s disease).

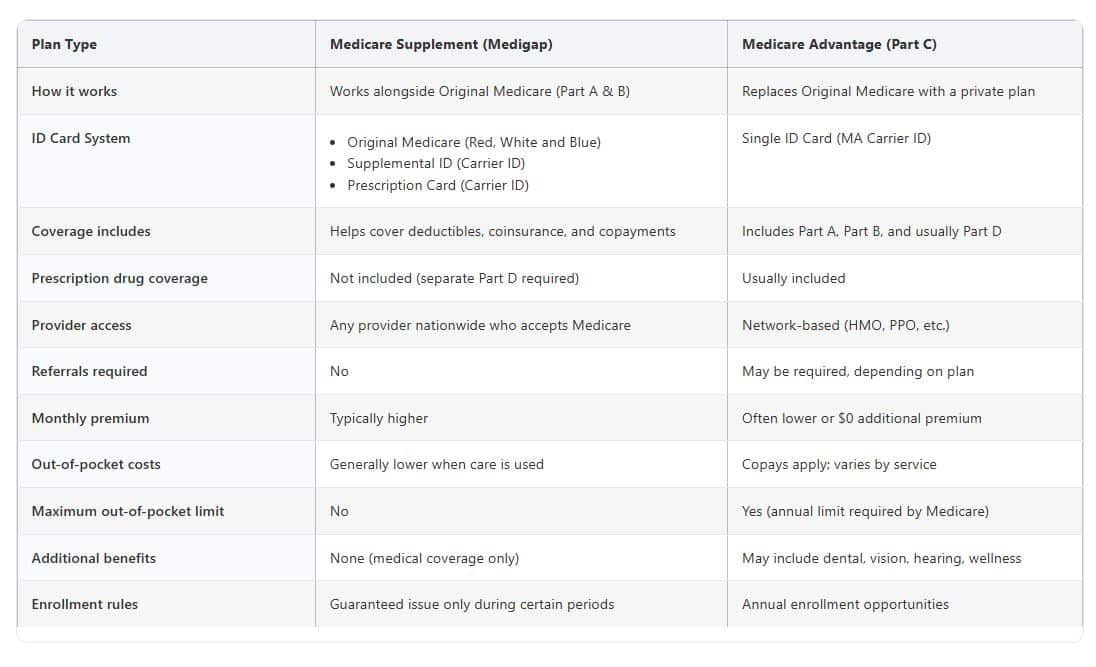

Below is a breakdown of the chart above.

| Plan Type | Medicare Supplement (Medigap) | Medicare Advantage (Part C) |

|---|---|---|

| How it works | Works alongside Original Medicare (Part A & B) | Replaces Original Medicare with a private plan |

| ID Card System |

|

Single ID Card (MA Carrier ID) |

| Coverage includes | Helps cover deductibles, coinsurance, and copayments | Includes Part A, Part B, and usually Part D |

| Prescription drug coverage | Not included (separate Part D required) | Usually included |

| Provider access | Any provider nationwide who accepts Medicare | Network-based (HMO, PPO, etc.) |

| Referrals required | No | May be required, depending on plan |

| Monthly premium | Typically higher | Often lower or $0 additional premium |

| Out-of-pocket costs | Generally lower when care is used | Copays apply; varies by service |

| Maximum out-of-pocket limit | No | Yes (annual limit required by Medicare) |

| Additional benefits | None (medical coverage only) | May include dental, vision, hearing, wellness |

| Enrollment rules | Guaranteed issue only during certain periods | Annual enrollment opportunities |

Medicare Supplement (Medigap)

Works alongside Original Medicare (Part A & B)

Medicare Advantage (Part C)

Replaces Original Medicare with a private plan

Medicare Supplement (Medigap)

Medicare Advantage (Part C)

Single ID Card (MA Carrier ID)

Medicare Supplement (Medigap)

Helps cover deductibles, coinsurance, and copayments

Medicare Advantage (Part C)

Includes Part A, Part B, and usually Part D

Medicare Supplement (Medigap)

Not included (separate Part D required)

Medicare Advantage (Part C)

Usually included

Medicare Supplement (Medigap)

Any provider nationwide who accepts Medicare

Medicare Advantage (Part C)

Network-based (HMO, PPO, etc.)

Medicare Supplement (Medigap)

No

Medicare Advantage (Part C)

May be required, depending on plan

Medicare Supplement (Medigap)

Typically higher

Medicare Advantage (Part C)

Often lower or $0 additional premium

Medicare Supplement (Medigap)

Generally lower when care is used

Medicare Advantage (Part C)

Copays apply; varies by service

Medicare Supplement (Medigap)

No

Medicare Advantage (Part C)

Yes (annual limit required by Medicare)

Medicare Supplement (Medigap)

None (medical coverage only)

Medicare Advantage (Part C)

May include dental, vision, hearing, wellness

Medicare Supplement (Medigap)

Guaranteed issue only during certain periods

Medicare Advantage (Part C)

Annual enrollment opportunities

Choosing the right Medicare coverage depends on several factors, including your health needs, travel habits, provider preferences, and budget. Medicare Advantage plans and Medicare Supplement plans each offer different benefits, and the best option varies from person to person.

At TMR & Associates, we help individuals understand Medicare, compare plan options, and make informed decisions with confidence. Whether you are new to Medicare or reviewing your current coverage, we are here to help guide you every step of the way.

Website & SEO By: MI Digital Solution